I usually spend a good chunk of my free time reading articles and listening to podcasts on software development, tech, and other industry news. Over the past few months, I’ve been spending a growing portion of that time learning about personal finance. At the time of this writing, I have just a few months left in college and at the beginning of this quarter the reality that I am soon going to be working full time started to sink in. At the same time, I began to realize how little I really knew about personal finance, so I decided to change that.

After getting some recommendations from a couple friends who are further along in life than I am, I dove deep into the world of personal finance. I began reading books, listening to podcasts, and following blogs. After a couple of weeks, it became a bit of an obsession and I was determined to learn everything I could about the subject before I start working and having a real income to manage and budget. Now, 3 books, over 100 hours of podcasts, and countless blog posts later, I’ve slowed down a bit and started to solidify the things that I am learning by putting them into practice and by sharing them with my friends and family.

If consuming all that personal finance literature has done one thing, it’s made me hyper-aware of the cashflows in my life. I’ve found that, like most people, the three largest categories in my spending are food, housing, and transportation. I plan to write posts about each of those categories, and in this first one I will be focusing on food. More specifically, I’ll be talking about choice of grocery store.

Where To Get Food

It’s often preached in the personal finance community that one of the fastest ways that most people can start saving extreme amounts of money very quickly is by choosing not to eat out and to cook at home. That shift away from eating out is the topic of a separate post, but chances are you’re like most people and you already cook at home and eat food from grocery stores for something between 40% and 90% of your meals, so you can certainly benefit from reduced grocery costs.

Reducing grocery spending has been on my mind a lot this week, so I decided to do a small experiment. There is a disproportionately high number of grocery stores next to the student apartments at UCLA, but the two I find myself at most frequently are Ralphs and Whole Foods. I like going to Whole Foods because of the free samples, the hot foods bar (which is actually more expensive to eat at than a lot of restaurants I go to), and most recently because they introduced 5% cash back for Amazon Prime Visa carriers. That being said, I do feel guilty whenever I am in Whole Foods because I know that it is widely considered to be outrageously expensive.

The goal of my experiment was to determine just how much more expensive Whole Foods is than Ralphs.

The Experiment

Methods

The set up was fairly simple. I planned to put together a shopping list, compare the prices for all of the items from Ralphs and from Whole Foods, and then extrapolate the results in order to determine how the price differences would affect my finances in the long run.

Prediction

My hypothesis was that Whole Foods would be more expensive, based on its reputation and a bit of personal experience, but I didn’t expect the difference to be too large. If it were small enough, it would probably be worth it for the slightly shorter walk to and from my apartment compared to Ralphs, I thought.

Collecting Data

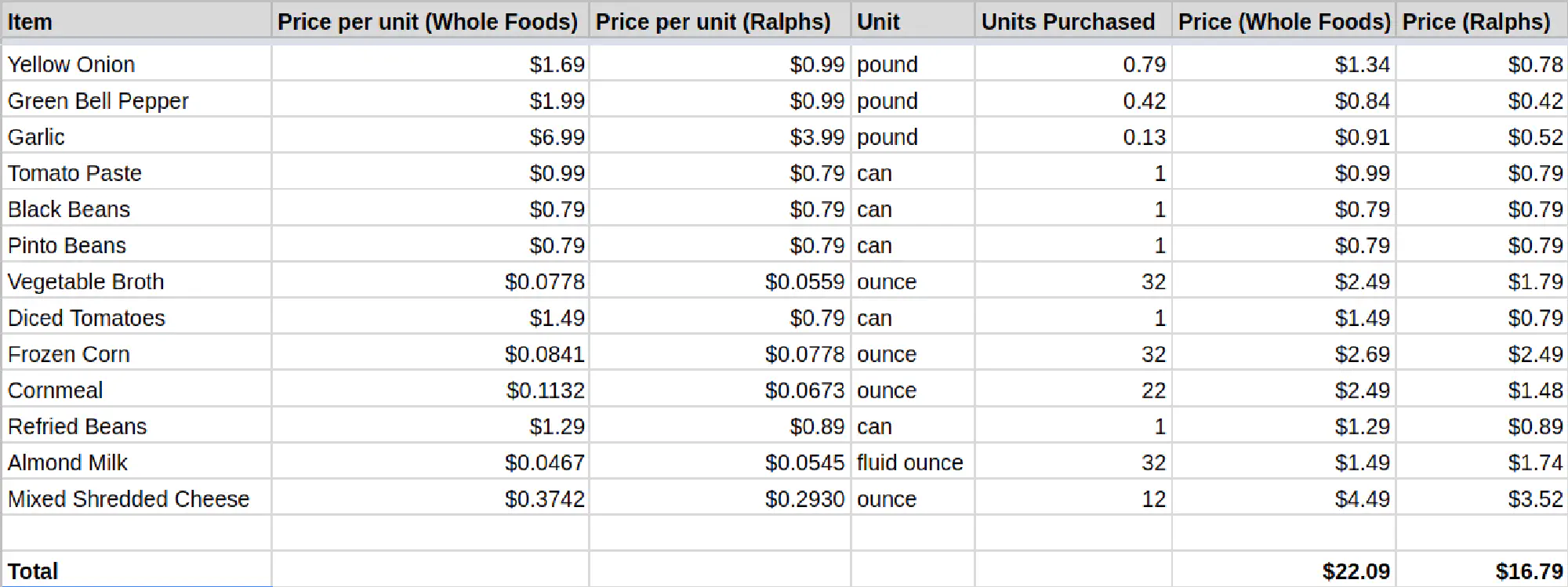

I put together a shopping list for a specific recipe that I was going to make. (Specifically, Joel Fuhrman’s Two Bean Chili from his Eat to Live cookbook, plus a few other things I needed to get.) I then went to both Ralphs and Whole Foods and recorded the prices of everything on my shopping list.

Results

When I got home, I plugged all the prices I had recorded in to a spreadsheet to compare the two grocery stores side-by-side.

The total cost at Ralphs was $16.79. The total cost at Whole Food was $22.09, which can be reduced to $20.99 after the 5% cash back from Amazon. This was certainly significant, but that $4.20 difference between Ralphs and Whole Foods might be worth the free samples and the shorter walk home, right?

Analysis

If we assume that the price ratios in this shopping list are representative of the price ratios for my average grocery visit, then we can extrapolate these results to see how they affect my spending and saving in the long term.

If I spend $300 per month on groceries at Ralphs, then that’s $3,600 per year. This would increase to $4,736 if I were to shop at Whole Foods instead. Put this way, that $1,136 difference doesn’t sound nearly as innocent as the $4.20 difference per-visit did!

That alone is more than enough reason for me to stick with Ralphs, but we can take this even further. Let’s say we invest that $1,136 each year at 10% annual interest. If I did that starting now, it will have grown to about $167,000 by the time I’m 50 (I’m 22 now). That’s a lot of money that could be put to much better use than a trip to Whole Foods (like pursuing Financial Independence and retiring a few years earlier).

Conclusion

These calculations were pretty surprising for me, and it’s suffice to say that I’ll be cutting out those infrequent trips to Whole Foods now. My methods and analysis were by no means exhaustive, and I made some ballpark assumptions in my calculations that could have certainly skewed the results. For example, the price ratios on that shopping list may actually be quite a bit different than a more representative sample of my grocery shopping, and to make this complete, I should really compare prices at the Trader Joe’s and Target by UCLA as well. Despite this, I don’t expect my conclusion that choosing to shop at Ralphs rather than Whole Foods is an undeniably great financial decision.

If you’d like to read more about saving money on food from people who are way more insightful and experienced than I am, I’d encourage you to check out this post from Early Retirement Extreme on Grocery Shopping and this podcast.

Thanks for reading!